Retirement is a time to finally embrace the freedom you’ve worked so hard to achieve, and for many, this includes the dream of living abroad. Whether it’s a beachfront property in Mexico, a charming villa in Europe, or simply the allure of exploring a new culture, retiring across borders has become an increasingly popular choice. However, achieving a financially secure retirement in another country requires careful planning and investment strategies tailored to your unique goals and circumstances. One such strategy involves leveraging mutual fund trusts to support your cross-border retirement aspirations.

Mutual fund trusts are an investment vehicle designed to pool money from multiple investors to purchase a diversified portfolio of securities. They are highly adaptable, offering exposure to a wide range of asset classes, including stocks, bonds, and real estate. This built-in diversification can help reduce risk while optimizing growth, which is especially important when planning for the complexities of retiring abroad.

For Canadians considering a cross-border retirement, mutual fund trusts offer several key advantages. First, they provide the opportunity to grow your wealth tax-efficiently while you’re still in Canada. Contributions to certain registered plans, such as an RRSP, can be invested in mutual fund trusts, allowing your investments to grow tax-deferred. This compounding effect can significantly enhance your retirement savings, giving you more financial flexibility when you make the move to your chosen destination.

Another advantage lies in the global reach of mutual fund trusts. Many funds offer exposure to international markets, enabling you to align your portfolio with the economy of the country where you plan to retire. For example, if your sights are set on Mexico, investing in funds with holdings in Latin American markets could provide a natural hedge against currency fluctuations while positioning your portfolio to benefit from regional economic growth. This strategic alignment can help smooth the transition from a Canadian-based retirement to a life abroad.

Liquidity is another critical feature of mutual fund trusts that makes them ideal for cross-border retirement planning. Unlike more illiquid investments, such as real estate or certain private equity funds, mutual fund trusts allow you to access your funds relatively quickly and without excessive penalties. This flexibility is essential for retirees who may need to adapt their plans or access capital for unexpected expenses, such as healthcare or currency shifts in their new country of residence.

Tax considerations are also central to cross-border retirement planning. Depending on the country where you choose to retire, the taxation of your investments and income may vary significantly. Mutual fund trusts, particularly those held in tax-advantaged accounts like an RRSP or TFSA, can help mitigate these complexities by offering a clear structure for growth and withdrawals. Understanding how double-taxation agreements and foreign tax credits apply to your investments can further enhance your ability to maximize your income while minimizing your liabilities.

Achieving a successful cross-border retirement requires more than just financial acumen—it demands a clear strategy that bridges your current financial reality with your future lifestyle goals. Mutual fund trusts provide a versatile and effective tool for building and sustaining the wealth needed to make those goals a reality. Their combination of diversification, global reach, liquidity, and tax efficiency makes them an ideal choice for retirees preparing to navigate the challenges and opportunities of living abroad.

At Seaport Credit, we specialize in helping clients like you plan for a fulfilling and financially secure cross-border retirement. Our team offers tailored strategies that integrate mutual fund trusts into a broader retirement plan designed to meet your unique needs. With Seaport Credit, you can approach your international retirement with confidence, knowing your finances are optimized to support the life you’ve always dreamed of.

Planning for retirement is one of the most significant financial goals most people will face, but when your dreams include retiring abroad, the process becomes even more complex—and exciting. Moving to another country to enjoy a lower cost of living, better weather, or a fresh start can enhance your golden years in countless ways. However, ensuring that you have the financial foundation to support this transition requires careful planning, especially when it comes to leveraging your Registered Retirment Savings Plan (RRSP) effectively. By using the right strategies, your RRSP can serve as a powerful tool for building wealth and providing financial security as you prepare for life beyond Canada’s borders.

An RRSP is one of the most versatile savings instruments available to Canadians. Contributions are tax-deductible, and the investments within the account grow tax-free until withdrawn. This dual advantage of tax deferral and compounded growth makes the RSP an excellent vehicle for maximizing retirement savings. However, optimizing its use requires more than just making annual contributions—you need to align your RRSP strategy with the specific financial considerations of retiring abroad.

The first step is to assess your long-term goals and financial needs. Retiring abroad often involves different living expenses than staying in Canada, and these variations can significantly impact your savings targets. For example, if you’re moving to a country with a lower cost of living, such as Mexico or Portugal, your retirement savings may stretch further. Conversely, if you’re eyeing a destination with higher healthcare costs or fluctuating currency values, you’ll need to account for those additional expenses.

Next, consider the tax implications of withdrawing RRSP funds while living abroad. Canada has tax treaties with many countries that dictate how your RRSP withdrawals will be taxed, both in Canada and your new country of residence. Understanding these treaties can help you minimize tax burdens and avoid unexpected liabilities. Working with a tax professional or financial advisor who specializes in cross-border retirement planning is highly recommended at this stage.

Diversification is another critical aspect of an effective RRSP strategy. While your RRSP may already hold a mix of investments, including equities, bonds, and mutual funds, retiring abroad might require rebalancing your portfolio to include assets that align with global markets or currencies. For instance, if you’re planning to live in Europe, holding investments tied to the Euro could provide a hedge against currency fluctuations. Additionally, real estate investments in your destination country could serve as both a home and a potential income source.

Timing your RRSP withdrawals is equally important. The key is to balance your need for income with tax efficiency. Structured withdrawals that take advantage of lower tax brackets can maximize your after-tax income. If you’re retiring early, consider converting a portion of your RSP into a Registered Retirement Income Fund (RRIF) to access funds gradually while keeping the rest of your savings sheltered.

Finally, don’t underestimate the importance of building a contingency fund outside of your RRSP. While your RRSP is designed for retirement, unforeseen expenses like medical emergencies, currency volatility, or changes in residency laws can arise. Having a separate pool of accessible, non-registered funds ensures that you’re prepared for any surprises without derailing your long-term financial plan.

At Seaport Credit, we understand that retiring abroad is more than just a financial decision—it’s a lifestyle transformation. Our team specializes in helping clients optimize their RRSPs and other savings tools to create wealth that supports their unique vision of retirement. Whether you’re drawn to the beaches of the Caribbean, the historic charm of Europe, or anywhere in between, Seaport Credit offers tailored strategies to ensure your journey is as financially secure as it is fulfilling. Trust us to guide you in turning your dream of retiring abroad into a reality.

Investing in MFTs (Mutual Fund Trusts) is a cornerstone strategy for building wealth, offering a combination of diversification, accessibility, and potential growth. Whether you’re saving for retirement, a major life event, or simply looking to grow your capital, mutual fund trusts can provide the framework for achieving your financial goals. However, one critical decision shapes the direction of your investment journey: should you choose active management or passive management? Each approach carries its own set of advantages and challenges, and understanding these differences is essential for making informed decisions.

Active management takes a hands-on approach to investing. Professional fund managers, supported by teams of analysts, continually assess market conditions, conduct in-depth research, and select securities they believe will outperform a specific benchmark. The promise of active management lies in its potential for higher returns. By identifying undervalued assets or leveraging short-term market opportunities, fund managers aim to achieve performance that surpasses the broader market. This strategy is particularly appealing in less efficient markets, where skilled managers can exploit anomalies that may not yet be priced into securities.

However, the pursuit of outperformance comes at a cost. Actively managed funds often charge higher fees, which can erode returns over time, particularly if the fund underperforms its benchmark. These fees are justified by the resources required for research and decision-making, but they make active funds less attractive to cost-conscious investors. Moreover, even the most experienced managers face challenges in consistently beating the market, especially in efficient markets where information is quickly absorbed and reflected in prices.

On the other hand, passive management offers a starkly different philosophy. Rather than trying to outguess the market, passive funds aim to replicate the performance of a specific index, such as the S&P/TSX Composite Index. This strategy provides a simple, cost-effective way to achieve market returns. With lower fees, fewer transactions, and minimal need for active oversight, passive funds are an attractive choice for investors seeking long-term growth without the complexities of active management.

While passive funds excel in terms of affordability and simplicity, they come with their own set of limitations. By design, these funds lack flexibility. They cannot adapt to changing market conditions or capitalize on opportunities to outperform the index they track. For investors seeking to minimize losses during market downturns or capitalize on specific growth opportunities, this rigidity can be a drawback.

Choosing between active and passive management depends on your financial goals, risk tolerance, and investment preferences. Active management may be suitable if you are looking for higher returns and are willing to take on additional costs and risks. Conversely, passive management is ideal for those seeking steady, predictable performance at a lower cost. Many investors opt for a balanced approach, combining active and passive funds to achieve diversification and leverage the strengths of both strategies.

For those navigating these choices, expert guidance can make all the difference. At Seaport Credit, we specialize in helping clients tailor their investment portfolios to their unique financial objectives. Whether you prefer the dynamic opportunities of active management, the cost-efficiency of passive funds, or a blend of both, our team provides the insights and strategies you need to optimize your investments. Trust Seaport Credit to guide you toward smarter financial decisions, ensuring that your mutual fund trust investments are aligned with your vision for the future.

An Exempt Market Dealer (EMD) is a registered securities dealer which facilitates trades in the private capital market. Investing in exempt markets can be an attractive option for those looking to diversify their portfolios beyond traditional stocks and bonds. These markets offer access to opportunities such as private equity, real estate developments, and alternative investments that are typically unavailable in public markets. However, navigating the complexities of exempt market investments requires a careful and informed approach. This is where the role of an exempt market dealer (EMD) becomes critical. Understanding what to expect during the due diligence process conducted by an EMD can help investors feel confident about their decisions and safeguard their investments.

The due diligence process conducted by an EMD is designed to protect investors by thoroughly vetting the investment opportunities they bring to market. This begins with a rigorous evaluation of the issuer, including their financial health, track record, and the management team’s expertise. EMDs scrutinize business plans, project viability, and market potential to ensure the offering is credible and well-structured. For instance, in real estate investments, an EMD would assess property valuations, location advantages, and development timelines to verify that the proposed project aligns with realistic financial projections.

A key part of the due diligence process also involves reviewing legal compliance. Exempt market investments operate under specific securities regulations that allow them to be sold without a prospectus. While this exemption offers flexibility, it also places a significant responsibility on the EMD to ensure that the investment complies with all applicable laws. This includes verifying that the issuer has met all disclosure requirements, adhered to securities regulations, and provided transparent information to potential investors.

Risk assessment is another critical component of due diligence. Unlike public markets, exempt market investments are less liquid and often carry higher risk. An EMD evaluates these risks by analyzing factors such as market volatility, economic conditions, and the potential for financial loss. The goal is to provide investors with a clear picture of the risks involved so they can make informed decisions. While no investment is without risk, the due diligence process helps mitigate exposure by eliminating poorly structured or overly speculative opportunities.

Communication with investors is equally important. A reputable EMD will ensure that all materials provided are comprehensive and easy to understand, from offering documents to risk disclosures. They will also take the time to address investor questions, clarify uncertainties, and ensure that each investor fully understands the nature of the investment. This transparency fosters trust and empowers investors to proceed with confidence.

For investors new to the exempt market space, the due diligence process may seem complex, but it’s a critical safeguard for ensuring that their investments are both legitimate and aligned with their financial goals. Whether you’re exploring opportunities in private equity, real estate, or other alternative investments, partnering with a trusted EMD is essential.

At Seaport Credit, we understand the importance of due diligence in exempt market investing. Our team of experts is committed to providing the highest standard of scrutiny for every opportunity we present, ensuring that your investments are not only compliant but also aligned with your unique financial objectives. With Seaport Credit as your guide, you can trust that your journey into exempt markets will be both secure and rewarding.

Western Pacific Trust is a well-established financial institution specializing in trust and corporate services tailored to meet diverse client needs. Their expertise spans a wide range of financial solutions, making them a trusted partner for individuals, families, and businesses seeking effective strategies to manage assets, secure investments, and plan for the future. By focusing on personalized service and innovative solutions, Western Pacific Trust has built a reputation for reliability and excellence.

At the core of their offerings are trust services, designed to help clients preserve and grow their wealth. These services include establishing personal and family trusts, which provide tax efficiency, asset protection, and estate planning benefits. Trusts ensure that wealth is transferred according to the client’s wishes while minimizing legal and financial complexities.

Western Pacific Trust also provides escrow services, acting as a neutral third party to facilitate secure transactions. This is particularly beneficial in real estate, mergers and acquisitions, or other high-value dealings where trust and transparency are paramount. By managing the flow of funds and ensuring that all conditions are met, they provide peace of mind to all parties involved.

Corporate services form another key pillar of their business. Western Pacific Trust supports businesses with corporate escrow solutions, shareholder services, and assistance with regulatory compliance.

Additionally, Western Pacific Trust’s self-directed account services empower individuals to take control of their retirement savings and investments. These accounts offer the flexibility to invest in a wide array of assets, including real estate, private equity, and other alternative investments, providing opportunities to diversify and optimize returns.

Navigating financial solutions such as those offered by Western Pacific Trust often requires access to capital and strategic planning. This is where Seaport Credit Canada can help. By providing tailored financing solutions and expert guidance, Seaport Credit supports Canadians looking to leverage services like trusts, escrow accounts, and self-directed investment opportunities. Whether you’re planning for the future, managing assets, or exploring new financial strategies, Seaport Credit Canada ensures you have the resources to succeed. With Seaport Credit by your side, you can maximize the benefits of working with institutions like Western Pacific Trust while confidently pursuing your financial goals.

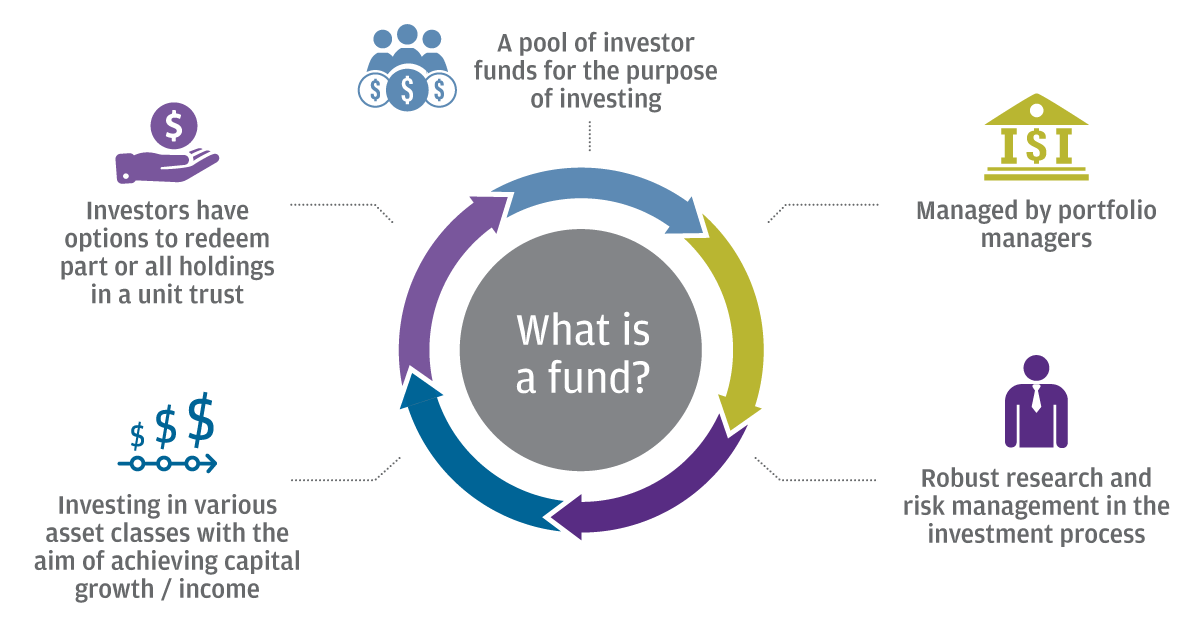

Mutual fund trusts are a popular investment vehicle for individuals looking to diversify their portfolios and achieve long-term financial growth. While the concept may seem complex at first, understanding the basics can help you make informed decisions about whether a mutual fund trust aligns with your financial goals.

At its core, a mutual fund trust pools money from multiple investors to buy a diversified mix of securities, such as stocks, bonds, and other assets. Unlike a mutual fund corporation, which is structured as a company with shares, a mutual fund trust operates under the legal framework of a trust, with the fund’s income distributed to investors (known as unitholders) in the form of units. This structure offers several benefits, including tax efficiency and flexibility.

One of the key advantages of a mutual fund trust is its ability to provide diversification. By spreading investments across various asset classes, sectors, and geographic regions, these funds help reduce risk while offering exposure to multiple growth opportunities. This makes mutual fund trusts an attractive option for beginner investors who may lack the expertise to build a well-rounded portfolio on their own.

Another benefit is professional management. Mutual fund trusts are managed by experienced portfolio managers who make investment decisions based on thorough market research and analysis. This expertise allows investors to access strategies that would be difficult or time-consuming to implement individually.

However, like all investments, mutual fund trusts come with potential risks. Market volatility, management fees, and taxation on distributions can impact overall returns. It’s essential to research fund performance, fee structures, and alignment with your financial objectives before investing. Understanding your risk tolerance and investment timeline will also guide your choice of funds, whether they lean toward growth, income, or a balanced strategy.

For Canadian investors seeking to explore mutual fund trusts or other investment opportunities, having access to the right financial tools and advice is crucial. Seaport Credit Canada offers tailored financial solutions to help you take the first step toward achieving your investment goals. Whether you’re starting a new portfolio or looking to optimize your current investments, Seaport Credit provides flexible credit options and expert guidance. With Seaport Credit Canada, you can confidently navigate the world of mutual fund trusts and build a financial future aligned with your aspirations.